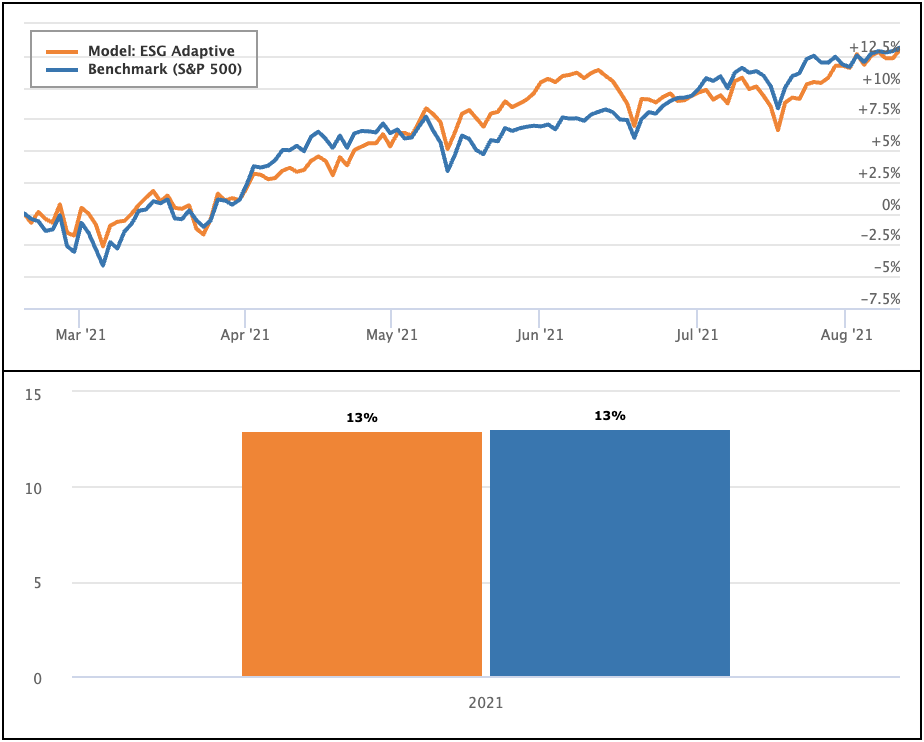

This long-only model portfolio is predicated on a pre-qualified set of ESG friendly constituents from the Russell 1000 and S&P 500.

Past performance is not indicative of future returns. Report generated on 8/11/2021.

0%

Annualized Return

0

Sharpe Ratio

0%

Drawdown

0

Beta

About this Strategy

The goal of the strategy is to outperform the SPXTR (SP 500 Total Return, which accounts for dividends, splits and reverse splits), in both total return and risk adjusted return (lower volatility). Every 21 days the model dynamically adjusts to the most recent market conditions — as measured by Neuravest data.

Past performance is not indicative of future returns.

Investment Approach

We use ranked technical and fundamental features normalized to market cap size and geared to identify abnormal inflection points relative to peers. The model retrains dynamically on a roll forward basis to account for changes in market regime.